QR Codes for Banks and Financial Services: ATM Queue, KYC, Statements, IBAN Sharing, and the MENA Open-Banking Playbookرموز QR للبنوك والخدمات الماليّة: تذكرة الصرّاف الآلي، اعرف عميلك، الكشوفات، مشاركة IBAN، وكتالوج المصرفيّة المفتوحة في الشرق الأوسط

Banks print billions of statements, operate thousands of ATMs, and serve hundreds of millions of mobile-banking customers across MENA. Every one of those touchpoints is a candidate for a QR — done right, QR routes ATM queues into the mobile app, embeds pay-this-bill actions into printed statements, lets customers share IBANs without typing 24 digits, and shortcuts KYC document submission from days to minutes. Done wrong, it leaks customer data, gets impersonated by financial quishing, and trains customers to scan every QR they see including the fake ones. This is the full banking-QR playbook: ten use cases across the customer journey, the SAMA / CBUAE / CBE / CBK regulatory layer, the open-banking integration patterns, the Vision 2030 banking-sector reform context, the anti-quishing posture banks specifically need, and the eight mistakes that turn a useful banking QR into a regulatory incident.البنوك تطبع مليارات الكشوفات، تشغّل آلاف أجهزة الصرّاف الآلي، وتخدم مئات الملايين من عملاء الخدمات المصرفيّة عبر الجوّال في الشرق الأوسط. كلّ نقطة لمس من هذه مرشّحة لرمز QR — إذا فُعل بشكل صحيح، يوجّه الرمز طوابير الصرّاف الآلي إلى تطبيق الجوّال، يضمّن إجراءات «ادفع هذه الفاتورة» في الكشوفات المطبوعة، يتيح للعملاء مشاركة IBAN دون كتابة ٢٤ رقماً، ويختصر تقديم وثائق «اعرف عميلك» من أيّام إلى دقائق. إذا فُعل بشكل خاطئ، يسرّب بيانات العملاء، يُنتحَل عبر التصيّد المالي، ويدرّب العملاء على مسح كلّ رمز يرونه بما في ذلك المزيّفة. هذا هو كتالوج QR المصرفي الكامل: عشر حالات استخدام عبر رحلة العميل، طبقة الجهات التنظيميّة (ساما، المركزي الإماراتي، المركزي المصري، المركزي الكويتي)، أنماط تكامل المصرفيّة المفتوحة، سياق إصلاح القطاع المصرفي في رؤية ٢٠٣٠، وضع مكافحة التصيّد الذي تحتاجه البنوك تحديداً، والأخطاء الثمانية التي تحوّل رمز QR مصرفي مفيد إلى حادثة تنظيميّة.

Banking is the single largest enterprise QR opportunity in the world that almost nobody writes about. Banks print billions of statements every year. They operate tens of thousands of ATMs and branches. They serve hundreds of millions of mobile-banking customers across MENA. Every one of those touchpoints — every statement, every ATM, every branch counter, every mailed letter, every push notification — is a candidate for a QR code that connects the physical-or-document layer of banking to the customer's mobile-banking app. Most of these QR opportunities are still unbuilt, and the banks that are building them are doing it in fragments — an isolated 'pay this bill' QR here, a queue-ticket kiosk there — without the cohesive playbook that the rest of this article is going to lay out.

This piece is the banking-QR playbook for MENA. It covers: ten distinct QR use cases across the customer banking journey, the regulatory layer that banking imposes that no other sector requires (SAMA, CBUAE, CBE, CBK, CBB data-residency and customer-data rules), how open-banking integration changes the QR pattern, the Vision 2030 banking-sector reform context driving demand, the heightened anti-quishing posture banks specifically need (because financial-services impersonation is the highest-impact fraud vector), and the eight mistakes that turn a useful banking QR into a regulatory incident. Banking is high-stakes — the features that make QR valuable here are the same features that make the failure modes serious.

Why banking is uniquely suited to QR

Three structural properties of retail banking make it the highest-value vertical for QR after healthcare.

First, the customer touches the bank constantly. A retail-bank customer in MENA transacts daily — checking balance, transferring money to family, paying SADAD/Fawateer bills, scanning IBANs to add beneficiaries, depositing salary, withdrawing cash at ATMs. The per-customer touchpoint count over a year is far higher than retail or hospitality. Every digitised friction-reduction at a touchpoint compounds across a relationship that lasts decades — banks have customer lifetimes of 15-30 years in MENA, where bank-switching friction is genuinely high.

Second, banks are document-heavy. Statements, account-opening forms, KYC certificates, loan applications, beneficiary-add forms, salary-letter requests, debit-card-issuance letters, complaint-resolution letters — the paper layer of banking is huge. Every printed document is a candidate to carry a QR that bridges the document to a mobile-banking action. The pattern in our PDF-QR guide applies at scale here, with banks being the highest-volume PDF-with-QR-embedded use case globally.

Third, the regulatory framework already pushes banks toward digital integration. SAMA's Open Banking framework in Saudi Arabia (Phase 1 live since 2023, Phase 2 expanding through 2026), the CBUAE Tom platform in UAE, the CBE digital-only bank licensing in Egypt, the CBK fintech sandbox in Kuwait — every Gulf central bank is actively building or has built infrastructure where QR sits naturally. A QR pointing at an Open-Banking-authenticated payment flow is doing real work in the regulatory architecture, not bolting onto an analogue process.

Ten QR use cases across the banking customer journey

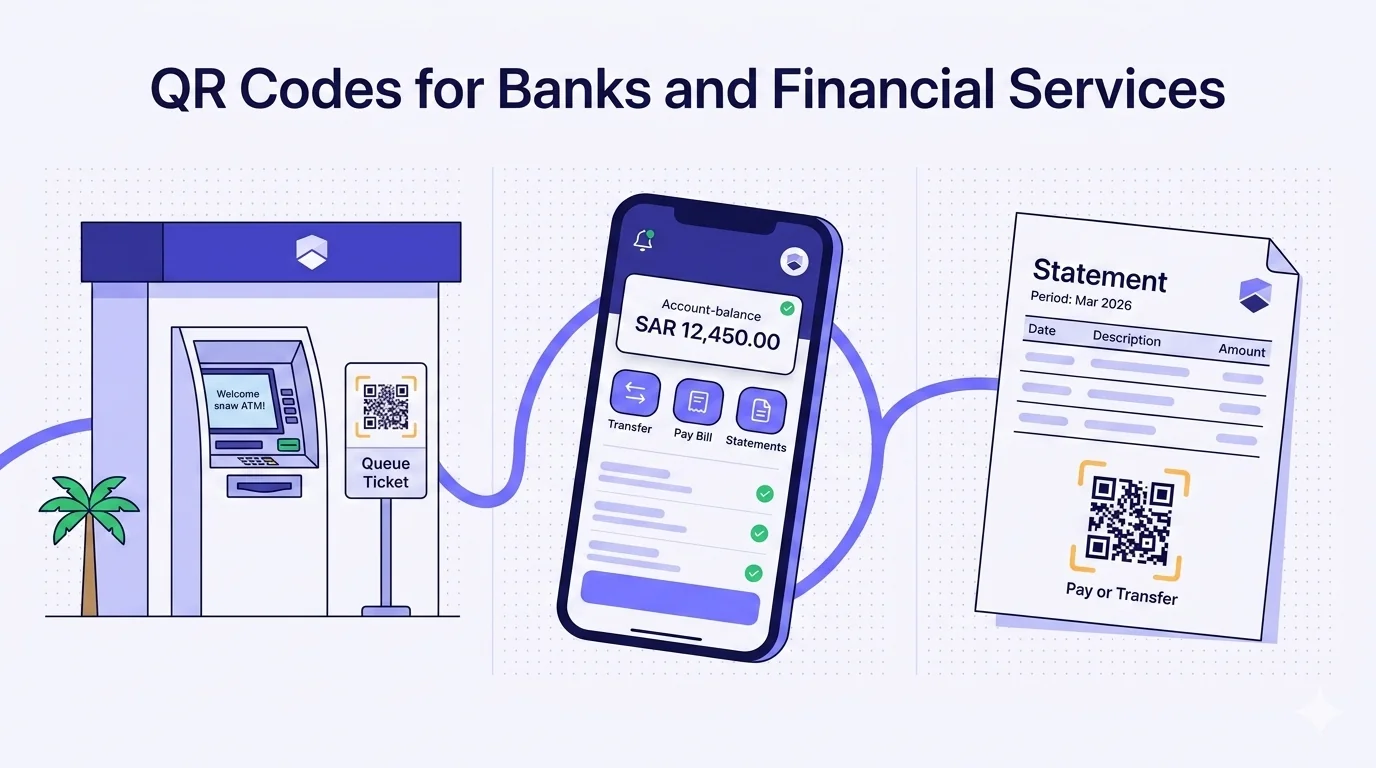

1 — ATM queue-ticket and self-service routing

Major branches in Riyadh, Jeddah, Dubai, Abu Dhabi, Cairo serve hundreds of customers a day. A QR at the entrance lets the customer self-issue a queue ticket from their phone — scan, confirm desired service (account opening, cash deposit, complaint, foreign exchange), receive a digital ticket and estimated wait time, optionally leave the branch and return when called. For the bank, this reduces front-desk congestion and lets walk-in volume be load-balanced into the mobile app. For the customer, it eliminates the 'sit in the branch for 45 minutes' experience. STC Pay, Al Rajhi, Emirates NBD, ENBD, CIB, NBE, Mashreq have all deployed variants of this pattern in their flagship branches.

2 — Statement-PDF pay-this-bill QR

Bank statements (whether emailed PDF or printed) typically list bills due, loan instalments, credit-card minimums. A QR on the statement that opens 'pay this directly in the app' eliminates the 5-step process of opening the app, navigating to bill-pay, entering the biller, entering the reference number, entering the amount, confirming. Scan → pre-filled payment screen → confirm with biometric → done. For credit-card statements specifically, scan-to-pay is the highest-value embedded action because credit-card minimums are time-sensitive (avoiding late fees) and the friction-reduction translates directly into reduced delinquency. The detail in our mada/MEEZA/KNET payments piece applies as the underlying payment-scheme layer.

3 — IBAN sharing QR

Every IBAN is 24 characters in Saudi Arabia (SA + 22 digits), and similar lengths in UAE, Egypt, Kuwait. Sharing an IBAN with someone who needs to send you money — for salary deposit at a new employer, for family transfers, for vendor payments — requires either copying 24 digits perfectly or sharing a long screenshot that the recipient then has to OCR or type manually. A QR encoding the IBAN as a payment-scheme reference (using ISO 20022 or SARIE/IPS-compatible encoding) lets the recipient scan once and have the IBAN auto-populated in their transfer screen. This is one of the highest-frequency banking interactions across MENA and one where the friction is currently embarrassingly high — every adult does this monthly.

4 — Beneficiary-add and trust-elevation QR

Adding a new beneficiary to a bank account typically requires the beneficiary's full name, IBAN, bank name, and SWIFT/BIC code, plus a 24-48-hour 'cooling period' before the beneficiary can receive transfers above small thresholds — a SAMA-imposed anti-fraud measure. A QR shared by the beneficiary (containing all required details plus an attested-by-the-sending-bank verification token) reduces the data-entry friction AND lets the receiving bank verify the beneficiary's identity through the QR's encoded trust chain, potentially shortcutting the cooling period for verified IBAN-to-IBAN transfers between mada-network accounts. This pattern is the natural next step in SAMA Open Banking Phase 2 rollout.

5 — KYC document submission

Onboarding to a new bank account, refreshing expired ID documents, updating residence proof — each KYC step requires the customer to physically present documents or submit them through a portal. A QR-driven KYC flow lets the customer scan a single QR (printed on the welcome letter, the renewal notice, or the in-branch document-required slip), open a secure upload page tied to their account, photograph the document with their phone's camera, and submit. The bank's compliance team reviews; if approved, the KYC status updates automatically. Saudi's NCAAA / Absher integration and UAE's Pass digital-ID platform both naturally connect to this pattern.

6 — Card issuance and activation QR

A new debit or credit card mailed to a customer typically requires an activation step — calling an IVR, logging into the app, sometimes both. A QR on the activation letter (or on the carrier the card ships in) that opens directly into the app's card-activation flow with the card token pre-populated eliminates the friction. Scan, confirm via biometric, card is active. Major issuers (Al Rajhi, SAB, Mashreq) have deployed variants; the pattern still has room to spread to smaller banks.

7 — Loan application initiation QR

Loan-product marketing — auto loans, home loans, personal loans, SME credit lines — is printed on branch posters, ATM screen ads, statement inserts, mailers. A QR on each loan-product marketing surface that opens directly into the application flow (pre-populated with what the customer's existing relationship with the bank already knows — name, IBAN, employer, salary band) cuts application abandonment dramatically. The 'I'll apply later when I'm at my laptop' moment is where most loan-product interest leaks; QR-to-app captures the interest before it cools.

8 — Bill payment (SADAD / Fawateer / NEPP) QR

MENA payment networks (Saudi SADAD, UAE eDirham/Fawateer, Egypt Fawry, Kuwait Knet bill-pay, Bahrain BenefitPay) all support QR-encoded biller-and-reference combinations. A printed utility bill, telco bill, government-fee invoice with a QR lets the customer scan and pay through whichever bank app they use. The QR encodes the biller ID, the reference number, and (for fixed-amount bills) the amount, so the customer's app pre-populates the payment screen. Egypt's Instant Payment Network (IPN, launched 2023) standardised QR-based bill payments at the network level; Saudi's IPS (Instant Payment System, replacing SARIE for retail) is doing the same. This is one of the most-volume QR use cases in MENA banking, by far.

9 — Complaint-and-escalation QR (SAMA, regulatory consumer protection)

SAMA mandates that Saudi banks provide customers with a complaint-escalation path that includes the option to escalate to SAMA directly if the bank doesn't resolve within 30 days. A QR on every customer-facing branch and document that opens the bank's complaint-submission portal (and from there, the SAMA escalation page) makes this consumer-protection layer accessible without the customer having to find the right URL on the bank's website. CBUAE has a similar requirement in UAE; CBE in Egypt.

10 — Customer-feedback / NPS-survey QR

After a branch visit, an ATM interaction, a call-centre conversation, a loan-application decision — a QR on the receipt, the exit signage, the SMS confirmation that opens a brief experience survey. For banks under regulatory quality frameworks (the SAMA banking customer experience index, the CBUAE customer treatment standard, the CBE consumer protection metrics), aggregated survey data feeds into the bank's regulatory standing. QR-based surveys triple response rates over the in-branch paper feedback box that nobody fills out.

The banking-specific regulatory layer

Customer data residency

Saudi customer banking data must reside in Saudi Arabia under SAMA's data-residency requirements. UAE customer banking data must reside in UAE under CBUAE. Egypt under CBE. These are non-negotiable for any QR whose destination touches customer-identifying information. A QR routing through a US-hosted redirect service is a regulatory violation even if the eventual destination is the bank's own app. Banks need QR infrastructure with in-country redirect hosting.

Authentication before sensitive content

A QR alone is not authentication. Anyone holding a printed bank statement could scan its QR. So sensitive destinations (statement details, payment confirmation, KYC document upload, beneficiary add) must require Strong Customer Authentication (SCA) before any content displays — at minimum a biometric or PIN entry in the bank app, ideally with a transaction-binding cryptographic confirmation. SAMA's Open Banking SCA framework, the EBA-equivalent CBUAE rules in UAE, and similar in Egypt, all impose specific SCA requirements that the QR's downstream destination must satisfy.

Anti-quishing — banking is the highest-impact fraud target

Financial-services impersonation via QR is the highest-impact quishing category. The defence stack: branded dynamic QRs with the bank's verified mark on every printed surface, customer education micro-copy ('Verify the URL is bankname.com before authenticating'), end-to-end domain-control of the redirect path, and monitoring of scan-anomaly patterns (sudden volume drops on a known-public-installation QR can indicate a sticker-overlay attack). The detail in our quishing safety primer applies — banks need the strongest version of every defence.

Audit trail and regulatory reporting

Every QR scan that leads to a customer-impacting action (payment, KYC submission, complaint, login) must be logged with the data points the regulator may request: timestamp, customer identity, scanning device, geographic source, action taken, success/failure, downstream confirmation. This is far stricter than retail or hospitality QR analytics. Banking QR platforms need audit-grade logging built in from the start, not retrofitted.

Open banking and the QR layer

SAMA Open Banking Phase 1 (account information services, live since 2023) and Phase 2 (payment initiation services, expanding through 2026) create new QR patterns. A third-party financial-services app authorised under Open Banking can issue a QR that, when scanned by the customer's bank app, initiates a payment from the customer's bank account to the third party — without the customer manually entering the third party's IBAN, amount, or reference. The QR encodes the Open Banking authorization token; the bank app validates against SAMA's authentication framework; the payment executes. This pattern is enabling the new wave of MENA fintech (STC Pay, Tabby, Tamara, Lean, MNT Halan, Telda) to offer 'scan to pay from your bank account' flows that were previously impossible.

The same pattern works for account-information requests: a budgeting app or a loan-broker app can issue a QR that, scanned by the customer, authorises the third party to read the customer's account history for a defined period. The scan establishes consent visibly (the customer sees what they're authorising), the Open Banking authorization establishes the right (the cryptographic permission token), and the bank's API delivers the data. Visual consent is the underrated piece — customers understand 'scan to authorize' far better than 'tap this consent toggle in the app's deep menu'.

Vision 2030 and the banking sector transformation

Saudi Arabia's Vision 2030 includes a financial-sector transformation programme — the Financial Sector Development Programme (FSDP) — that's reshaping the entire banking layer at unprecedented scale. New digital-only banks (STC Bank, D360, EmkanBank), expanded fintech licensing (the SAMA fintech sandbox graduating dozens of licensed players), mada+ rollout (the next-generation mada payment scheme with extended QR capabilities), instant-payments evolution (SARIE → IPS), and Open Banking Phase 2 are all on multi-year rollouts ending mid-late 2026. Every one of these initiatives has a QR layer. New digital-only banks specifically lean heavily on QR-driven onboarding, IBAN-sharing, and bill-pay as their core friction-reduction value proposition versus the established universal banks. The detail in our mada/MEEZA/KNET payments piece and ZATCA Phase 2 piece applies as adjacent regulatory context.

Eight mistakes that turn banking QR into a regulatory incident

- Destination is hosted outside the country where the customer data resides. SAMA, CBUAE, CBE all reject this. In-country hosting is non-negotiable for any QR touching customer-identifying data.

- QR opens a customer-data page without Strong Customer Authentication. Holding the printed statement should not grant access to the statement details. Always require biometric/PIN authentication before content displays.

- Static QR encoding a fixed URL on a long-lived printed surface. Banks reorganise URL structures, migrate systems, replace platforms — every 2-3 years. Dynamic QR through a bank-controlled redirect prevents the statement-QR-now-points-to-nowhere failure.

- No anti-quishing posture on customer-facing physical surfaces. Branch QRs, ATM-sticker QRs, statement QRs are all sticker-overlay-attack targets. Branded frames, surveillance for stickers in public locations, customer education micro-copy.

- QR encoding customer name or account number in the QR payload itself. The data is visible to anyone scanning. Encode an opaque token that only the bank's backend can resolve to customer identity.

- No audit logging on QR scans that lead to customer-impacting actions. When the regulator audits, you can't reconstruct the action's chain. Build audit logging in from the start.

- Generic third-party QR-generator tool used without data-residency and audit-grade controls. The QR works but the supplier is a regulatory liability. Banks need banking-grade QR infrastructure.

- No customer-education layer alongside the QR rollout. Customers who haven't been taught how to verify the QR's authenticity will scan any sticker that looks like a bank QR. The fraud campaigns specifically target untrained customer bases.

How QRA handles banking-grade workflows

QRA QRs are dynamic by default, hosted on infrastructure with in-region data residency for MENA banking deployments, brand-framed for bank identity (the bank's logo on every QR), authentication-gated for sensitive destinations, audit-log-instrumented for regulator-grade traceability, and analytics-instrumented so banks can see scan-source patterns including fraud-anomaly detection. The bulk-create workflow handles the volume — banks needing to generate one QR per statement, one per branch, one per ATM, one per card-issuance letter, can run tens of thousands of QRs through a single CSV-import operation. Integration with downstream core-banking systems is via the destination-URL pattern: each QR points at an internal bank endpoint that the QRA dashboard editable-redirect can re-point if the bank migrates platforms or restructures URLs. For Open-Banking-integrated flows, the QR can carry an Open Banking authorization token in the URL fragment, satisfying SAMA's consent-and-authentication requirements end-to-end.

The short answer

Banking is the highest-value enterprise QR vertical after healthcare because banks have the most touchpoints, the highest document volume, and the strongest regulatory pull toward digital integration. Ten use cases span the customer journey: ATM queue, statement-pay, IBAN share, beneficiary add, KYC submission, card activation, loan application, bill payment, complaint escalation, NPS survey. The compliance overhead is the strictest of any sector — in-country data residency, Strong Customer Authentication on sensitive destinations, audit-grade logging, anti-quishing defence, customer education. Vision 2030 banking transformation (FSDP, Open Banking Phase 2, mada+, digital-only banks) is driving multi-year demand for banking-grade QR infrastructure. Done well, QR cuts customer friction at every touchpoint; done poorly, it becomes a SAMA / CBUAE / CBE incident. Branded, dynamic, authenticated, audit-logged, and in-jurisdiction — those are the five non-negotiables for banking.

القطاع المصرفي هو أكبر فرصة QR مؤسّسيّة منفردة في العالم لا يكتب عنها أحد تقريباً. البنوك تطبع مليارات الكشوفات سنويّاً. تشغّل عشرات الآلاف من أجهزة الصرّاف الآلي والفروع. تخدم مئات الملايين من عملاء المصرفيّة عبر الجوّال في الشرق الأوسط. كلّ نقطة لمس من هذه — كلّ كشف، كلّ صرّاف، كلّ طاولة فرع، كلّ رسالة بريديّة، كلّ إشعار دفع — مرشّحة لرمز QR يربط الطبقة الفيزيائيّة أو الوثائقيّة للبنوك بتطبيق المصرفيّة الجوّالة للعميل. معظم فرص QR هذه لا تزال غير مبنيّة، والبنوك التي تبنيها تفعل ذلك على شكل قطع متفرّقة — رمز معزول «ادفع هذه الفاتورة» هنا، كشك تذكرة طابور هناك — دون الكتالوج المتكامل الذي سيرسمه هذا المقال.

هذا المقال هو كتالوج QR المصرفي للشرق الأوسط. يغطّي: عشر حالات استخدام QR متمايزة عبر رحلة العميل المصرفي، الطبقة التنظيميّة التي يفرضها القطاع المصرفي ولا يفرضها أيّ قطاع آخر (متطلّبات إقامة البيانات وقواعد بيانات العملاء لساما، المركزي الإماراتي، المركزي المصري، المركزي الكويتي، المركزي البحريني)، كيف يغيّر تكامل المصرفيّة المفتوحة نمط QR، سياق إصلاح القطاع المصرفي في رؤية ٢٠٣٠ الذي يقود الطلب، وضع مكافحة التصيّد المرتفع الذي تحتاجه البنوك تحديداً (لأنّ انتحال الخدمات الماليّة أعلى ناقل احتيال تأثيراً)، والأخطاء الثمانية التي تحوّل QR مصرفي مفيد إلى حادثة تنظيميّة. القطاع المصرفي عالي المخاطر — الخصائص نفسها التي تجعل QR قيّماً هنا هي ما يجعل أنماط الفشل خطيرة.

لماذا القطاع المصرفي مناسب فريداً لرمز QR

ثلاث خصائص بنيويّة للمصرفيّة الأفراد تجعله أعلى قطاع قيمة QR بعد القطاع الصحي.

أوّلاً، العميل يلامس البنك باستمرار. عميل مصرفيّة أفراد في الشرق الأوسط يجري معاملات يوميّاً — فحص الرصيد، تحويل الأموال للعائلة، دفع فواتير سداد/فواتير، مسح آيبان لإضافة مستفيدين، إيداع راتب، سحب نقد عند الصرّاف الآلي. عدد نقاط اللمس للعميل عبر السنة أعلى بكثير من التجزئة أو الضيافة. كلّ تقليل احتكاك مرقمن في نقطة لمس يتراكم عبر علاقة تستمرّ عقوداً — البنوك لها عمر علاقة عميل ١٥-٣٠ سنة في الشرق الأوسط، حيث احتكاك تبديل البنك مرتفع فعلاً.

ثانياً، البنوك مكثّفة الوثائق. كشوفات، نماذج فتح حساب، شهادات «اعرف عميلك»، طلبات قروض، نماذج إضافة مستفيد، طلبات شهادات راتب، رسائل إصدار بطاقات الخصم، رسائل حلّ شكاوى — الطبقة الورقيّة للقطاع المصرفي هائلة. كلّ وثيقة مطبوعة مرشّحة لحمل QR يجسر الوثيقة إلى إجراء مصرفيّة جوّال. النمط في دليل QR للـPDF ينطبق على نطاق واسع هنا، مع كون البنوك أعلى حالة استخدام بحجم لـPDF مع QR مُضمَّن عالميّاً.

ثالثاً، الإطار التنظيمي يدفع البنوك نحو التكامل الرقمي. إطار المصرفيّة المفتوحة لساما في السعوديّة (المرحلة ١ حيّة منذ ٢٠٢٣، المرحلة ٢ تتوسّع خلال ٢٠٢٦)، منصّة Tom للمركزي الإماراتي، ترخيص البنوك الرقميّة فقط للمركزي المصري في مصر، منصّة الاختبار الرملي للتقنيّة الماليّة في الكويت — كلّ بنك مركزي خليجي يبني أو بنى بنية تحتيّة حيث يقع QR طبيعيّاً. رمز يشير إلى تدفّق دفع مُصادَق عليه بالمصرفيّة المفتوحة يؤدّي عملاً حقيقيّاً في المعماريّة التنظيميّة، لا يُربَط فوق عمليّة تماثليّة.

عشر حالات استخدام QR عبر رحلة العميل المصرفي

١ — تذكرة طابور الصرّاف الآلي والتوجيه الذاتي

الفروع الكبرى في الرياض، جدّة، دبي، أبوظبي، القاهرة تخدم مئات العملاء يوميّاً. رمز عند المدخل يتيح للعميل إصدار تذكرة طابور ذاتيّاً من هاتفه — مسح، تأكيد الخدمة المطلوبة (فتح حساب، إيداع نقد، شكوى، صرف عملات)، استلام تذكرة رقميّة ووقت انتظار مقدَّر، اختياريّاً مغادرة الفرع والعودة عند المناداة. للبنك، يقلّل ذلك ازدحام مكتب الاستقبال ويسمح بتوزيع الحضور الفوري إلى تطبيق الجوّال. للعميل، يُلغي تجربة «اجلس في الفرع ٤٥ دقيقة». STC Pay، الراجحي، Emirates NBD، CIB، NBE، Mashreq جميعها نشرت متغيّرات من هذا النمط في فروعها الرئيسيّة.

٢ — رمز «ادفع هذه الفاتورة» على كشف الحساب PDF

كشوفات البنوك (سواء PDF بالبريد أو مطبوعة) تذكر عادةً الفواتير المستحقّة، أقساط القروض، الحدود الدنيا لبطاقات الائتمان. رمز على الكشف يفتح «ادفع هذا مباشرةً في التطبيق» يُلغي العمليّة المؤلّفة من ٥ خطوات: فتح التطبيق، التنقّل إلى دفع الفواتير، إدخال الفوترة، إدخال الرقم المرجعي، إدخال المبلغ، التأكيد. مسح ← شاشة دفع مُعبَّأة مسبقاً ← تأكيد ببصمة حيويّة ← تمّ. لكشوفات بطاقات الائتمان خاصّةً، المسح-للدفع أعلى إجراء مُضمَّن قيمةً لأنّ الحدود الدنيا لبطاقات الائتمان حسّاسة للوقت (تجنّب رسوم التأخير) ويُترجَم تقليل الاحتكاك مباشرةً إلى تقليل التأخّر عن السداد. التفاصيل في مقال مدى/ميزا/كي نت تنطبق كطبقة نظام الدفع الأساسيّة.

٣ — رمز مشاركة آيبان

كلّ آيبان ٢٤ حرفاً في السعوديّة (SA + ٢٢ رقماً)، وأطوال مماثلة في الإمارات، مصر، الكويت. مشاركة آيبان مع شخص يحتاج إرسال نقود إليك — لإيداع راتب لدى صاحب عمل جديد، لتحويلات عائليّة، لدفعات للموردين — تتطلّب إمّا نسخ ٢٤ رقماً بشكل مثالي أو مشاركة لقطة شاشة طويلة يضطرّ المستلم بعدها لاستخراج النصّ أو الكتابة يدويّاً. رمز يخزّن الآيبان كمرجع نظام دفع (باستخدام ISO 20022 أو ترميز متوافق مع SARIE/IPS) يتيح للمستلم المسح مرّة واحدة ويُعبّأ الآيبان تلقائيّاً في شاشة التحويل لديه. هذه واحدة من أعلى تكرارات التفاعل المصرفي في الشرق الأوسط وحيث الاحتكاك حاليّاً مرتفع بشكل محرج — كلّ بالغ يفعل هذا شهريّاً.

٤ — رمز إضافة مستفيد ورفع الثقة

إضافة مستفيد جديد إلى حساب بنكي تتطلّب عادةً اسم المستفيد الكامل، آيبانه، اسم البنك، ورمز SWIFT/BIC، إضافةً إلى فترة تبريد ٢٤-٤٨ ساعة قبل أن يستطيع المستفيد استلام تحويلات فوق عتبات صغيرة — إجراء مكافحة احتيال مفروض من ساما. رمز يشاركه المستفيد (يحوي كلّ التفاصيل المطلوبة إضافةً إلى رمز تحقّق موثَّق من البنك المُرسِل) يقلّل احتكاك إدخال البيانات ويتيح للبنك المستقبِل التحقّق من هويّة المستفيد عبر سلسلة الثقة المُشفَّرة في الرمز، ربّما مختصراً فترة التبريد للتحويلات من آيبان إلى آيبان بين حسابات شبكة مدى المُتحقَّق منها. هذا النمط هو الخطوة التالية الطبيعيّة في إطلاق المرحلة ٢ من المصرفيّة المفتوحة لساما.

٥ — تقديم وثائق «اعرف عميلك»

الانضمام إلى حساب بنكي جديد، تجديد وثائق هويّة منتهية، تحديث إثبات الإقامة — كلّ خطوة «اعرف عميلك» تتطلّب من العميل إحضار وثائق فيزيائيّاً أو تقديمها عبر بوّابة. تدفّق «اعرف عميلك» المدفوع بـQR يتيح للعميل مسح رمز واحد (مطبوع على رسالة الترحيب، إشعار التجديد، أو قسيمة «الوثيقة مطلوبة» داخل الفرع)، فتح صفحة رفع آمنة مرتبطة بحسابه، تصوير الوثيقة بكاميرا هاتفه، والتقديم. فريق الامتثال في البنك يراجع؛ إن وُوفِق، تتحدّث حالة «اعرف عميلك» تلقائيّاً. تكامل NCAAA / أبشر في السعوديّة ومنصّة الهويّة الرقميّة Pass في الإمارات يرتبطان طبيعيّاً بهذا النمط.

٦ — رمز إصدار وتفعيل البطاقة

بطاقة خصم أو ائتمان جديدة تُرسَل بالبريد إلى عميل تتطلّب عادةً خطوة تفعيل — اتّصال بـIVR، تسجيل دخول في التطبيق، أحياناً كلاهما. رمز على رسالة التفعيل (أو على غلاف شحن البطاقة) يفتح مباشرةً في تدفّق تفعيل البطاقة في التطبيق مع رمز البطاقة مُعبَّأ مسبقاً يُلغي الاحتكاك. مسح، تأكيد ببصمة حيويّة، البطاقة نشطة. كبار المصدّرين (الراجحي، SAB، Mashreq) نشروا متغيّرات؛ النمط لا يزال لديه مجال للانتشار إلى البنوك الأصغر.

٧ — رمز بدء طلب القرض

تسويق منتجات القروض — قروض السيّارات، قروض المنازل، القروض الشخصيّة، خطوط الائتمان للشركات الصغيرة — يُطبَع على ملصقات الفروع، إعلانات شاشة الصرّاف الآلي، إدراج الكشوفات، البريد المباشر. رمز على كلّ سطح تسويق منتج قرض يفتح مباشرةً في تدفّق الطلب (مُعبَّأ مسبقاً بما تعرفه علاقة العميل القائمة مع البنك أصلاً — الاسم، الآيبان، صاحب العمل، شريحة الراتب) يقطع التخلّي عن الطلب بشكل كبير. لحظة «سأقدّم لاحقاً حين أكون عند حاسوبي» هي حيث يتسرّب معظم الاهتمام بمنتج القرض؛ QR-إلى-التطبيق يلتقط الاهتمام قبل أن يبرد.

٨ — رمز دفع الفواتير (سداد / فواتير / NEPP)

شبكات الدفع في الشرق الأوسط (سداد السعودي، فواتير/eDirham الإماراتي، فوري المصري، Knet bill-pay الكويتي، BenefitPay البحريني) كلّها تدعم تركيبات مُسجَّلة-وفاتورة-ومرجع بـQR. فاتورة مرافق مطبوعة، فاتورة اتّصالات، إيصال رسوم حكوميّة برمز يتيح للعميل المسح والدفع عبر أيّ تطبيق بنك يستخدمه. الرمز يخزّن معرّف الفاتورة، الرقم المرجعي، و(للفواتير ذات المبلغ الثابت) المبلغ، فيُعبّأ تطبيق العميل شاشة الدفع مسبقاً. شبكة الدفع الفوري المصريّة (IPN، أُطلقت ٢٠٢٣) وضعت معياراً لدفع الفواتير المبني على QR على مستوى الشبكة؛ نظام الدفع الفوري السعودي (IPS، يحلّ مكان SARIE للأفراد) يفعل الشيء نفسه. هذه واحدة من أكثر حالات استخدام QR حجماً في القطاع المصرفي في الشرق الأوسط، بفارق كبير.

٩ — رمز الشكوى والتصعيد (ساما، حماية المستهلك التنظيميّة)

ساما تلزم البنوك السعوديّة بتوفير مسار تصعيد شكاوى للعملاء يشمل خيار التصعيد إلى ساما مباشرةً إن لم يحلّ البنك خلال ٣٠ يوماً. رمز على كلّ فرع ووثيقة موجّهة للعميل يفتح بوّابة تقديم الشكاوى في البنك (ومنها صفحة تصعيد ساما) يجعل طبقة حماية المستهلك هذه متاحة دون اضطرار العميل لإيجاد الرابط الصحيح على موقع البنك. المركزي الإماراتي لديه متطلّب مماثل في الإمارات؛ المركزي المصري في مصر.

١٠ — رمز ملاحظات العميل/استطلاع NPS

بعد زيارة فرع، تفاعل صرّاف آلي، محادثة مركز اتّصال، قرار طلب قرض — رمز على الإيصال، لافتة المخرج، تأكيد الرسالة القصيرة يفتح استطلاع تجربة موجزاً. للبنوك تحت أطر جودة تنظيميّة (مؤشّر تجربة العملاء المصرفي لساما، معيار معاملة العملاء للمركزي الإماراتي، مقاييس حماية المستهلك للمركزي المصري)، بيانات الاستطلاع المجمّعة تغذّي الموقف التنظيمي للبنك. استطلاعات QR تضاعف معدّلات الاستجابة ثلاثاً عن صندوق الملاحظات الورقي داخل الفرع الذي لا يملؤه أحد.

الطبقة التنظيميّة الخاصّة بالقطاع المصرفي

إقامة بيانات العملاء

بيانات المصرفيّة للعملاء السعوديّين يجب أن تقيم في السعوديّة وفق متطلّبات إقامة البيانات لساما. بيانات المصرفيّة للعملاء الإماراتيّين يجب أن تقيم في الإمارات وفق المركزي الإماراتي. مصر وفق المركزي المصري. هذه غير قابلة للتفاوض لأيّ رمز وجهته تلامس معلومات تعريف العميل. رمز يمرّ عبر خدمة إعادة توجيه مستضافة في الولايات المتّحدة هو انتهاك تنظيمي حتّى لو كانت الوجهة النهائيّة تطبيق البنك نفسه. البنوك تحتاج بنية QR بإعادة توجيه مستضافة داخل البلد.

المصادقة قبل المحتوى الحسّاس

QR وحده ليس مصادقة. أيّ شخص يحمل كشف حساب مطبوع يستطيع مسح رمزه. لذا الوجهات الحسّاسة (تفاصيل الكشف، تأكيد الدفع، رفع وثيقة «اعرف عميلك»، إضافة مستفيد) يجب أن تتطلّب مصادقة العميل القويّة (SCA) قبل عرض أيّ محتوى — كحدّ أدنى إدخال بصمة حيويّة أو رقم سري في تطبيق البنك، مثاليّاً مع تأكيد تشفيري يربط بالمعاملة. إطار SCA للمصرفيّة المفتوحة في ساما، قواعد المركزي الإماراتي المكافئة لـEBA في الإمارات، ومثلها في مصر، كلّها تفرض متطلّبات SCA محدّدة يجب أن تفي بها وجهة الرمز التالية.

مكافحة التصيّد — القطاع المصرفي أعلى هدف احتيال تأثيراً

انتحال الخدمات الماليّة عبر QR هو أعلى فئة تصيّد تأثيراً. مكدّس الدفاع: رموز QR ديناميكيّة موسومة بعلامة البنك المُتحقَّق منها على كلّ سطح مطبوع، نصّ تعليمي صغير موجَّه للعميل («تحقّق أنّ الرابط هو bankname.com قبل المصادقة»)، التحكّم الكامل بالنطاق من البداية إلى النهاية لمسار إعادة التوجيه، ومراقبة أنماط شذوذ المسح (انخفاضات حجم مفاجئة على رمز معروف في تركيب عامّ قد تشير إلى هجوم ملصق فوق ملصق). التفاصيل في دليل أمان QR والتصيّد تنطبق — البنوك تحتاج أقوى نسخة من كلّ دفاع.

أثر التدقيق والإبلاغ التنظيمي

كلّ مسح QR يقود إلى فعل يؤثّر على العميل (دفع، تقديم «اعرف عميلك»، شكوى، تسجيل دخول) يجب أن يُسجَّل بنقاط البيانات التي قد يطلبها المنظّم: الطابع الزمني، هويّة العميل، جهاز المسح، المصدر الجغرافي، الفعل المُتَّخَذ، النجاح/الفشل، تأكيد التالي. هذا أصرم بكثير من تحليلات QR التجزئة أو الضيافة. منصّات QR المصرفيّة تحتاج تسجيل من درجة التدقيق مبني من البداية، لا مُضافاً لاحقاً.

المصرفيّة المفتوحة وطبقة QR

المرحلة ١ من المصرفيّة المفتوحة لساما (خدمات معلومات الحسابات، حيّة منذ ٢٠٢٣) والمرحلة ٢ (خدمات بدء الدفع، تتوسّع خلال ٢٠٢٦) تخلقان أنماط QR جديدة. تطبيق خدمات ماليّة طرف ثالث مرخَّص ضمن المصرفيّة المفتوحة يستطيع إصدار رمز يبدأ، حين يُمسح بتطبيق بنك العميل، دفعاً من حساب العميل المصرفي إلى الطرف الثالث — دون إدخال العميل يدويّاً لآيبان الطرف الثالث، المبلغ، أو المرجع. الرمز يخزّن رمز تفويض المصرفيّة المفتوحة؛ تطبيق البنك يتحقّق مقابل إطار مصادقة ساما؛ الدفع ينفّذ. هذا النمط يمكّن الموجة الجديدة من التقنيّة الماليّة في الشرق الأوسط (STC Pay، Tabby، Tamara، Lean، MNT Halan، Telda) من تقديم تدفّقات «امسح للدفع من حسابك المصرفي» التي كانت مستحيلة سابقاً.

النمط نفسه يعمل لطلبات معلومات الحساب: تطبيق ميزانيّة أو تطبيق وسيط قروض يستطيع إصدار رمز، حين يُمسح بالعميل، يفوّض الطرف الثالث لقراءة تاريخ حساب العميل لفترة محدّدة. المسح يثبّت الموافقة بصريّاً (العميل يرى ما يفوّض)، تفويض المصرفيّة المفتوحة يثبّت الحقّ (رمز إذن تشفيري)، وواجهة برمجة تطبيقات البنك تسلّم البيانات. الموافقة البصريّة هي الجزء الأقلّ تقديراً — العملاء يفهمون «امسح للتفويض» أفضل بكثير من «اضغط مفتاح التبديل لهذه الموافقة في القائمة العميقة للتطبيق».

رؤية ٢٠٣٠ وتحوّل القطاع المصرفي

رؤية ٢٠٣٠ السعوديّة تشمل برنامج تحوّل القطاع المالي — برنامج تطوير القطاع المالي (FSDP) — الذي يعيد تشكيل الطبقة المصرفيّة بأكملها على نطاق غير مسبوق. بنوك رقميّة فقط جديدة (STC Bank، D360، EmkanBank)، توسيع ترخيص التقنيّة الماليّة (منصّة الاختبار الرملي للتقنيّة الماليّة في ساما تخرّج عشرات اللاعبين المرخَّصين)، إطلاق مدى+ (الجيل التالي من نظام دفع مدى بقدرات QR موسّعة)، تطوّر المدفوعات الفوريّة (SARIE → IPS)، والمرحلة ٢ من المصرفيّة المفتوحة، كلّها على إطلاقات متعدّدة السنوات تنتهي منتصف-أواخر ٢٠٢٦. كلّ واحدة من هذه المبادرات لها طبقة QR. البنوك الرقميّة فقط تحديداً تعتمد بقوّة على الانضمام المدفوع بـQR، مشاركة الآيبان، ودفع الفواتير كعرض قيمتها الأساسي لتقليل الاحتكاك مقابل البنوك الشاملة المرسَّخة. التفاصيل في مقال مدى/ميزا/كي نت ومقال ZATCA المرحلة ٢ تنطبق كسياق تنظيمي مجاور.

ثمانية أخطاء تحوّل QR المصرفي إلى حادثة تنظيميّة

- الوجهة مستضافة خارج البلد حيث تقيم بيانات العميل. ساما، المركزي الإماراتي، المركزي المصري كلّهم يرفضون هذا. الاستضافة داخل البلد غير قابلة للتفاوض لأيّ رمز يلامس بيانات تعريف العميل.

- QR يفتح صفحة بيانات عميل دون مصادقة قويّة. حمل الكشف المطبوع يجب ألّا يمنح وصولاً إلى تفاصيل الكشف. اطلب دائماً مصادقة ببصمة حيويّة/رقم سري قبل عرض المحتوى.

- رمز ثابت يخزّن رابطاً ثابتاً على سطح مطبوع طويل الأمد. البنوك تعيد تنظيم بنى الروابط، تهاجر أنظمة، تستبدل منصّات — كلّ ٢-٣ سنوات. رمز ديناميكي عبر إعادة توجيه يتحكّم بها البنك يمنع فشل «رمز الكشف يشير الآن إلى لا شيء».

- لا وضع مكافحة تصيّد على الأسطح الفيزيائيّة الموجّهة للعملاء. رموز الفروع، رموز ملصقات الصرّاف الآلي، رموز الكشوفات كلّها أهداف هجوم ملصق فوق ملصق. إطارات موسومة، مراقبة الملصقات في المواقع العامّة، نصّ تعليمي صغير موجَّه للعميل.

- QR يخزّن اسم العميل أو رقم حسابه في حمولة الرمز نفسه. البيانات مرئيّة لأيّ شخص يمسح. خزّن رمزاً غامضاً يستطيع خادم البنك وحده حلّه إلى هويّة العميل.

- لا تسجيل تدقيق على مسحات QR التي تقود إلى أفعال تؤثّر على العميل. حين يدقّق المنظّم، لا تستطيع إعادة بناء سلسلة الفعل. ابنِ تسجيل التدقيق من البداية.

- أداة QR-مولّد عامّة من طرف ثالث مستخدَمة دون ضوابط إقامة بيانات ودرجة تدقيق. الرمز يعمل لكنّ المورد عبء تنظيمي. البنوك تحتاج بنية QR من درجة مصرفيّة.

- لا طبقة تثقيف للعميل إلى جانب إطلاق QR. العملاء الذين لم يُعلَّموا كيف يتحقّقون من مصداقيّة الرمز سيمسحون أيّ ملصق يبدو كرمز بنك. حملات الاحتيال تستهدف تحديداً قواعد العملاء غير المدرَّبة.

كيف تتعامل QRA مع تدفّقات من درجة مصرفيّة

رموز QRA ديناميكيّة افتراضيّاً، مستضافة على بنية مع إقامة بيانات داخل المنطقة لعمليّات نشر مصرفيّة في الشرق الأوسط، موسومة بهويّة البنك (شعار البنك على كلّ رمز)، محميّة بالمصادقة للوجهات الحسّاسة، مجهّزة بسجلّ تدقيق لقابليّة تتبّع من درجة المنظّم، ومجهّزة بالتحليلات بحيث تستطيع البنوك رؤية أنماط مصدر المسح بما في ذلك كشف شذوذ الاحتيال. تدفّق الإنشاء الجماعي يعالج الحجم — البنوك التي تحتاج توليد رمز لكلّ كشف، رمز لكلّ فرع، رمز لكلّ صرّاف آلي، رمز لكلّ رسالة إصدار بطاقة، يمكنها تشغيل عشرات الآلاف من الرموز عبر عمليّة استيراد CSV واحدة. التكامل مع أنظمة الخدمات المصرفيّة الأساسيّة التالية عبر نمط رابط الوجهة: كلّ رمز يشير إلى نقطة نهاية داخليّة للبنك يستطيع إعادة توجيه قابلة للتعديل في لوحة QRA إعادة توجيهها إن هاجر البنك منصّات أو أعاد هيكلة الروابط. لتدفّقات المصرفيّة المفتوحة المتكاملة، الرمز يستطيع حمل رمز تفويض المصرفيّة المفتوحة في جزء الرابط، مُحقّقاً متطلّبات الموافقة والمصادقة لساما من البداية إلى النهاية.

الإجابة المختصرة

القطاع المصرفي هو أعلى قطاع قيمة QR مؤسّسي بعد القطاع الصحي لأنّ البنوك لديها أكثر نقاط لمس، أعلى حجم وثائق، وأقوى جذب تنظيمي نحو التكامل الرقمي. عشر حالات استخدام تمتدّ على رحلة العميل: طابور الصرّاف الآلي، الدفع من الكشف، مشاركة الآيبان، إضافة مستفيد، تقديم «اعرف عميلك»، تفعيل البطاقة، طلب القرض، دفع الفواتير، تصعيد الشكوى، استطلاع NPS. عبء الامتثال أصرم من أيّ قطاع — إقامة بيانات داخل البلد، مصادقة قويّة على الوجهات الحسّاسة، تسجيل من درجة التدقيق، دفاع مكافحة التصيّد، تثقيف العميل. تحوّل القطاع المصرفي في رؤية ٢٠٣٠ (FSDP، المرحلة ٢ من المصرفيّة المفتوحة، مدى+، البنوك الرقميّة فقط) يقود طلباً متعدّد السنوات على بنية QR من درجة مصرفيّة. إذا فُعل جيّداً، QR يقطع احتكاك العميل في كلّ نقطة لمس؛ إذا فُعل سيّئاً، يصبح حادثة ساما/المركزي الإماراتي/المركزي المصري. موسوم، ديناميكي، مُصادَق عليه، مُسجَّل تدقيقاً، وداخل الولاية القضائيّة — هذه هي الخمسة غير القابلة للتفاوض للقطاع المصرفي.

Ready to make a smarter QR?جاهز لإنشاء رمز QR أذكى؟

Sign up free — no card needed. Track every scan, edit destinations anytime.سجّل مجاناً — بدون بطاقة. تتبّع كل عملية مسح وعدّل الوجهة في أي وقت.